✏️ Explanatory Question

Answer with Explanation

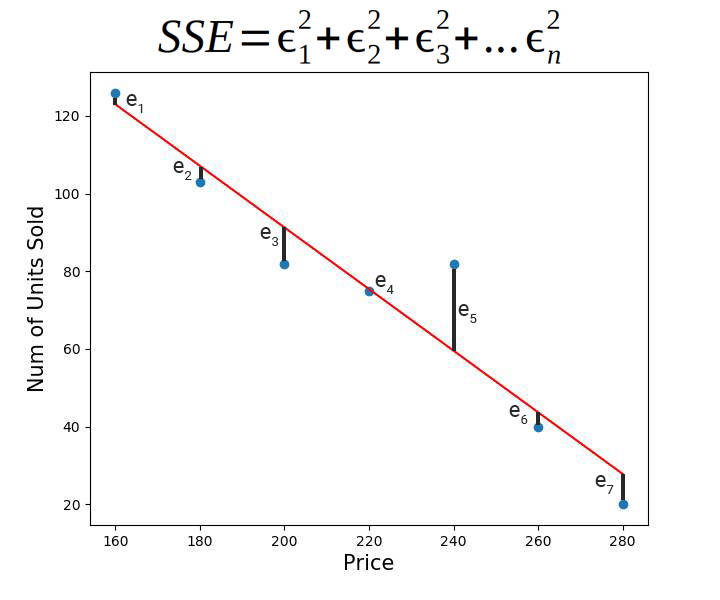

The Sum of Squared Errors (SSE) is a measure of how well a regression line fits a set of data points. It is calculated as the sum of the squared differences between the predicted values and the actual values of the dependent variable.

The reason why we calculate the SSE as squared differences is to give greater weight to larger errors. Squaring the differences amplifies the effect of large errors, while reducing the effect of small errors. This is desirable because we want our regression line to be as close as possible to the actual data points, particularly to those with larger errors, since those are the points that have a greater impact on the overall fit of the line.

In other words, squaring the errors helps to penalize larger errors more heavily than smaller errors, which can help to produce a better fit between the regression line and the data.

Furthermore, the squared errors also ensure that the SSE is always positive or zero, which is important for mathematical and statistical reasons.

In short, squaring the errors in the SSE calculation is a way to emphasize the importance of larger errors and to produce a more accurate measure of how well the regression line fits the data.